What is Debt?

Let’s begin by defining the term “debt”. According to Wikipedia:

“Debt is an obligation that requires one party, the debtor, to pay money or other agreed-upon value to another party, the creditor.”

Debt is not exactly a modern invention; it goes back as far as 3,500 B.C. when people used clay tablets as a record of a future obligation to pay.

In modern time, we use other forms of written contracts, but the concept of debt remains the same.

Featured Course

Fundamentals of Financial Analysis

Good Debt vs. Bad Debt

Good Debt

Good debt can be understood as debt that helps us build wealth. This means when we spend money on things that generate more income than we pay interest.

For example, suppose we obtain a loan for $100,000 for which you pay 4% interest annually. If you can invest that money and yield a return of 7%, you will make a profit of 3%.

After one year, you will have increased your wealth by $3,000.

Provided the interest rate does not outpace the level of return, taking on debt is a good idea.

Obtaining a loan to buy a car is considered good debt if it allows you the means to get to work or perform your work.

Bad Debt

Bad debt is debt that reduces your wealth; buying things you may not need or buying things that don’t generate income with money you don’t have.

Buying a new phone, TV, or vacation cruise on credit because you can’t afford it right now is a bad idea.

Other than immediate gratification, this type of debt doesn’t yield any other form of return, especially if you purchase these types of items on your credit card. You could be looking at paying high interest rates if your monthly balance is not paid.

You should only buy these types of things when you have saved enough and can really afford the purchase.

Businesses and Debt

Most businesses require assets to provide their customers with goods and services. These assets usually cost money, and these assets usually need to be financed.

The money can come from the owners of the business in which case Equity is put into the business.

Unfortunately, this money the owners put into the business is not enough and the business needs to obtain external financing, such as a bank loan.

The same principle of Good and Bad Debt applies here, too.

If the investment the business is using the money for is generating more return than it’s paying interest, it’s considered Good Debt; it’s increasing the wealth of the company.

Let me show you how taking on debt (or financial leverage) can be a good way to grow a business faster.

Featured Course

Power Excel Bundle

A Practical Example of Financial Leverage

Suppose you wish to operate a lemonade stand. To keep things simple, we won’t be factoring in any taxation.

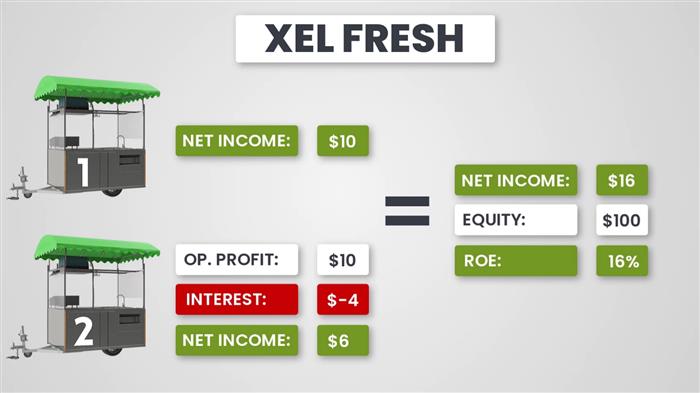

We begin by investing $100 of our own money as Equity into the business to be able to buy the assets you need, like the stand, equipment, and inventory (got to have lemons) you need to produce the lemonade.

After selling lemonade for a time, you manage to make a profit (net income) of $10.

In business terms, your Return on Equity (RoE = Profit / Equity) is 10%.

Because you managed to get a good return, you want to grow the business. In this example, it means launching another lemonade stand with another $100 investment.

At this point you have two options:

- You can wait until you have generated enough cash from the first stand to finance the second stand with your own money. This is known as “bootstrapping”.

- Obtain a loan from a bank for $100. This means you will take on debt.

You decide to go with the loan option because you see the opportunity to grow and you don’t want to wait.

The bank wants to make money as well, so they will charge you interest for the money they will give you. In this example, we’ll say they are charging you 4%.

You will incur an interest expense of $4 for the second lemonade stand.

The operating profit of the second stand is also $10. When we deduct the $4 interest expense you make a net income of $6.

Together with the first stand, you now have a net income of $16.

The equity which was your own money that you put into the business remains $100. This means that your Return on Equity (RoE) is 16%.

Working with other people’s money improved your RoE.

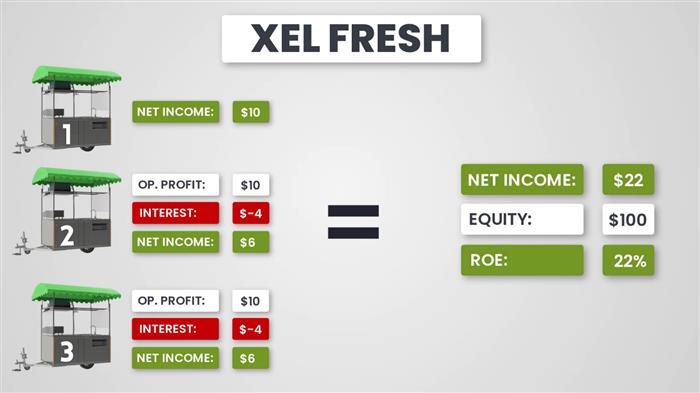

Because business is great and you want to grow further, you again go to the bank to get another loan of $100 at 4% interest.

The third stand makes the same profit as the first two stands; a profit of $10 minus $4 for interest gives you a net income of $6.

When combined with the other two stands you have a net income of $22 on your $100 equity. The RoE is now 22%.

By taking advantage of the leverage effect, you managed to more than double your RoE.

Featured Course

Excel Essentials for the Real World

Let’s Keep Up the Good Times

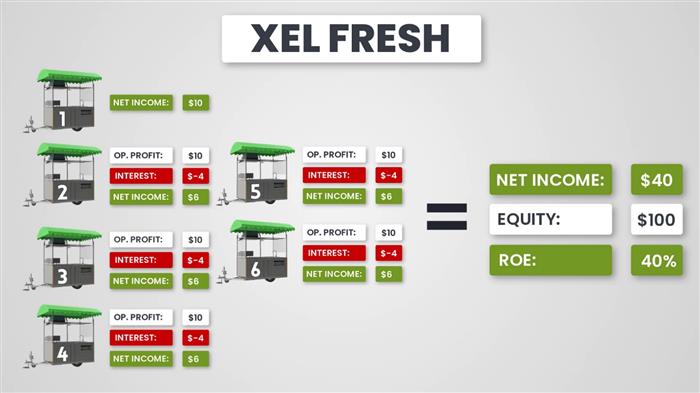

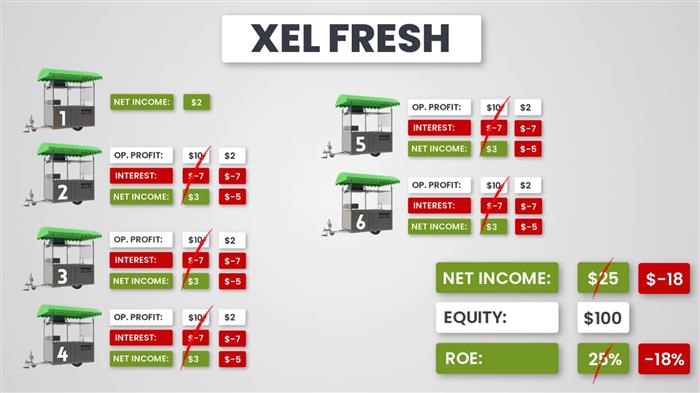

Because things are going so well, you go back to the bank, obtain more loans, open more stands, and keep making more and more money.

In no time at all, you are operating six stands with an RoE of 40%. Life is GREAT!

Can this story really be this simple? What’s stopping you from taking on more dept and opening more stands to become a world-wide lemonade conglomerate?

There are a few reasons why this has a practical limit.

- While leverage can help a business make money faster, you must be aware that debt always carries risk.

After the creation of six stands, the business has loans of $500 on its balance sheet, and at some point it will need to pay back this debt.

Provided it is warm and sunny, the business is profitable. What happens after an unusually rainy summer and the demand for lemonade is low? What if you need to go into lockdown do to an “unspecified virus of unknown origin”, will you even make enough profit to pay for the loans?

A highly leveraged company is always in a greater position of risk.

- Because your highly leveraged business will be considered higher risk, banks will be reluctant to open additional lines of credit to help you grow.

Even if you can obtain the additional loans, you will likely pay a higher interest rate because the bank will want to earn more for taking on a riskier loan.

The interest rate will not stay at the original 4%. This makes the loan more expensive and will reduce your profit margin.

Let’s say the bank offers a revised interest rate of 7% for funding $500 to open the additional stands.

You are now facing an additional interest expense of $15 (going from $4 to $7 in interest per stand) which reduces your net income to $25 (from $40).

Your RoE has been reduced from 40% down to 25%.

Granted, this is still better than only having one stand financed with pure equity earning 10%.

Enter the Competition

Suppose a competing lemonade stand opens next to yours. Your competition is quite experienced and operates many other stands around the world.

Because of their higher volume in purchases, they get lower prices for the lemons and oranges, so they can be more aggressive (i.e., lower) on the prices for the lemonade.

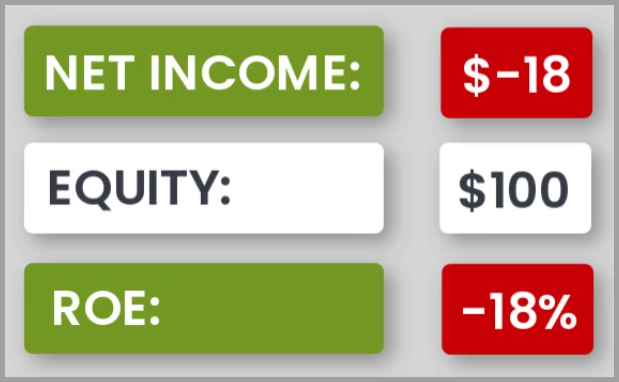

To not lose your customers, you are required to lower your prices resulting in a lower operating profit. Now you’re only making an operating profit of $2.

How does it affect the business?

If you only had the one lemonade stand, fully financed with equity, your RoE would be 2% on the $100 investment. Not great, but still better than just placing your money in a traditional savings account.

But you took on a lot of debt to finance your growth.

Now, for the additional five lemonade stands financed with bank loans, you have interest expenses to pay that are higher than your profits. Remember, operating profit is only $2 per stand with the revised sale prices, and with 7% interest rate for each $100 loan you must pay $7 interest leaving you with a loss of $5 for each lemonade stand.

This is not where the bad news ends. Because of the lack of profit, you don’t generate cash, so you can’t even pay back the interest.

You must finance the loss with more loans to remain solvent.

This won’t last long and soon your lemonade business will become a footnote in history.

Conclusion

Leverage allows companies to earn income from assets they normally wouldn’t be able to afford.

In good time, it can help you grow faster. It can multiply every dollar of your own money that you put into the business.

In bad times, it can leverage your losses and puts the business at risk to go down just as fast.

Leila Gharani

I'm a 6x Microsoft MVP with over 15 years of experience implementing and professionals on Management Information Systems of different sizes and nature.

My background is Masters in Economics, Economist, Consultant, Oracle HFM Accounting Systems Expert, SAP BW Project Manager. My passion is teaching, experimenting and sharing. I am also addicted to learning and enjoy taking online courses on a variety of topics.